Water & Wastewater Municipal Service Corporation

Background

In the evolving landscape of water and wastewater services, the creation of an MSC is an opportunity for the City and Utilities Kingston to improve service levels, enhance operational efficiency and foster sustainable practices.

Looking to the future, the city is facing significant growth, with a projected population increase to 220,900 by 2051, requiring 29,300 new homes. This growth occurs amid a housing crisis, climate emergency, and economic uncertainty, prompting the city to proactively plan. Utilities Kingston and the City have identified essential infrastructure projects to support this growth, which exceed their current financial and human resource capacities. To address these challenges, the City is exploring the establishment of Municipal Services Corporations (MSCs) to enhance operational and financial capabilities, endorsed by the provincial government and Association of Municipalities of Ontario.

What is a Municipal Services Corporation (MSC)?

An MSC is created by a municipality to manage specific services or assets. An MSC can only provide a system or a service that the municipality would provide and is created under the provisions of Ontario Regulation 599/06 under the Municipal Act, 2001.

Get Involved

- Learn more about the proposed organizational and financial structure

Ask a question using the Q&A tool below

-

Public Engagement Summary: Public MSC

Why we engaged

In the evolving landscape of water and wastewater services, the creation of a public MSC is an opportunity for the City and Utilities Kingston to support a faster pace for asset replacement and new infrastructure to meet growing needs while reducing financial impact on other municipal services such as roads and recreation services. Under Ontario’s Municipal Act, 2001 and Regulation 599/06, municipalities are authorized to establish public MSCs for delivering municipal services.

Public consultation with respect to the proposed public MSC model is required under Ontario Regulation 599/06.

The feedback summarized below reflects the range of comments received during consultation. In response to the feedback, the Public MSC Business Case has been updated to provide additional analysis, clarification, and supporting information.

How we engaged

The engagement period began on Dec. 4 2025. Community members were invited to read the KPMG Business Case, which outlined context and drivers for the proposal, details on the proposed governance structure, financial considerations and an overview of an implementation plan. A short survey provided an opportunity for residents to provide feedback on the business case, and there was a Q&A tool for participants to ask questions.

The engagement was promoted on Get Involved Kingston and on the City of Kingston and Utilities’ Kingston’s websites. A news release was distributed to media and news subscribers and the survey was included in social media posts on the City’s LinkedIn, Facebook, X and Instagram channels.

Residents were also given the opportunity to submit feedback offline and via email/CRM. An additional update that included detailed information about the proposed organizational structure, agreements, and financial models was published on Jan. 12. The survey was extended until Jan. 19, 2026.

Who we heard from

- 385 participants completed the survey*

- 30 questions asked using the Q&A tool

- 1,941 participants visited the project page to learn more

- 30 participants engaged with the City for the first time on Get Involved Kingston

- 825 downloads of the MSC Business Case

- 63,996 social media impressions

- 1,819 social media engagements

- 67 social media comments received**

- 13 CRM/emails sharing feedback on the proposal for an MSC

Locations of participants

- 25% Southwest Kingston (K7M)

- 39% Central-East Kingston (K7K)

- 7% Northwest Kingston (K7P)

- 24% Central-South Kingston (K7L)

- 4% Rural Kingston and Frontenac County (K0H)

- Less than 1% Other/outside of Kingston (L9G, A1C)

*Survey results are not statistically representative of the entire community, as engaged participants account for less than 0.29% of the total population of Kingston.

** Comments received on social media are not included in the public engagement summary. Statistics are provided to indicate community interest and social media reach.

What we heard

Most engagement participants told us they were somewhat familiar (68%) or not familiar (17%) with a public MSC model. After reading the business case, respondents shared that they are not supportive of the proposed public MSC. When asked about the strategic advantages of a public MSC, survey respondents consistently disagreed with all the strategic advantages offered in the business case. In open-ended feedback received in the survey and through emails and CRM submissions, respondents cited concerns about privatization, affordability, and transparency.

Figure A: Familiarity with a public MSC model

Figure B: Support of public MSC

Figure C: Agreement with Strategic Advantages

Summary of Feedback Themes (312 comments)

Summary of Feedback Themes (312 comments)Preference for current model and opposition to Privatization of Water Wastewater Services: A dominant theme is participant concern that a public MSC opens the door to privatization or profit-driven motives for essential services. Residents emphasize that water is a public good and must remain publicly owned and publicly managed. Many believe that if improvements are required they could be made within the existing water wastewater structure.

Accountability and Transparency: Many respondents worry that a public MSC reduces oversight by Council and residents. Concerns include nontransparent decision making, weaker public reporting and lack of accountability in cases of service failure or rate increases.

Skepticism of Business Case, Financial Uncertainty and Population Projections: Comments highlight a perceived lack of clear financial justification, missing comparisons to current model, minimal risk assessment and concerns about hidden liabilities and long-term cost implications. Some respondents questioned the population projections underpinning the rationale for change. Other respondents ask for case studies, performance data from other municipalities, and analyses of alternative approaches.

Concern about Impact on Rates and Affordability: Some respondents are concerned that a public MSC will lead to higher user fees, new charges, or cost-shifting that could disproportionately impact low-income residents.

Concern about risks to Service Quality and Public Health: Participants worry that a business-oriented approach could negatively affect water quality. Some cite international examples (notably the U.K.) and past crises (such as Walkerton) as warning that privatization can lead to reduced maintenance, environmental harm and compromised safety.

Insufficient Public Engagement: Some commenters criticize the public engagement process, stating they felt rushed and did not have the information needed to engage meaningfully.

Support and Positive Feedback: A few respondents are open to and/or supportive of a public MSC model, recognizing that population growth may require a new approach. Many supportive comments are conditional, emphasizing the need for clear governance, strong accountability and transparency, and insurance that the model remain fully publicly owned.

-

Additional MSC Information

Many questions have been received regarding the structure of the MSC and concerns about City Council’s control.

The proposed MSC would be a not-for-profit corporation which means that it reinvests all revenues into the water and wastewater operations and infrastructure. The MSC Board would be composed of various members of the community, with expertise in various areas, and representation from City Council. This is in line with a report produced by the Association of Municipalities of Ontario.

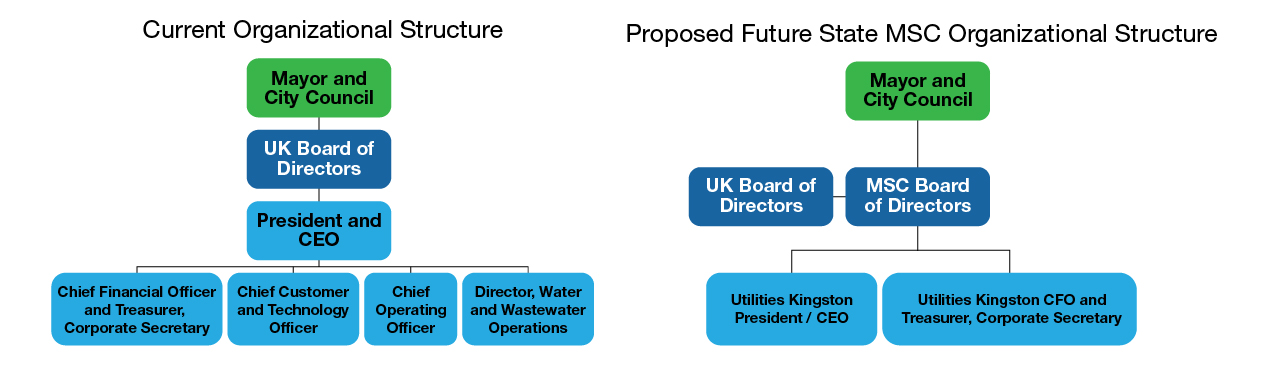

The illustration outlines the management and leadership structures of the current Utilities Kingston model and the proposed future state MSC model. Mayor & Council are and would continue to be sole shareholder under current and future proposed structure. The W/WW Operating MSC size would not justify a full-time President and CEO. Therefore, the appointment of the Utilities Kingston’s CEO would ensure coordination between the Utilities Kingston and the MSC during and following the transfer of assets from the City to the MSC; and of the day-to-day operations and management responsibilities which would continue as status quo under the leadership of the Utilities Kingston President and CEO.

The transition of the delivery of water and wastewater services from Utilities Kingston to the MSC would involve minimal organizational disruption. The primary changes include the termination of the existing service agreement between Utilities Kingston and the City, which would be replaced by a new agreement with the MSC. The MSC would also establish a service agreement with Utilities Kingston.

Figure A: Comparison of current and proposed organizational structures

Shareholder Agreement, Master Services Agreement & Administrative Agreement

A number of agreements would be in place between the City and the new MSC. The Shareholder agreement would sets parameters within which the MSC Board is permitted to operate independently. This Shareholder agreement would require City Council approval before the MSC board is established and operating. The Shareholder Agreement operates to bind the MSC to certain performance obligations, decision-making processes, development approval processes involving applicable infrastructure, and operational standards.

A Master Services Agreement between Council, Utilities Kingston and the MSC will mirror a contract for service, i.e., the scope and standards of services to be provided, clear performance metrics, regulatory compliance, reporting obligations, term and renewals, dispute resolution, and the calculation of the cost of service, including operational and capital considerations. It is important to note that under the existing Utilities Kingston governance model, the City Council has already relinquished its responsibilities pertaining to direct oversight of safe operations.

To the extent that the MSC will operationally remain the responsibility of Utilities Kingston, then an Administrative Services Agreement should be established between the MSC and Utilities Kingston. This allows for all of the day-to-day functions (e.g., operations, finance, human resources, information technology, customer service, etc.) to be carried out by management and employees of Utilities Kingston on behalf of the MSC.

Similar to a Master Services Agreement, the Administrative Services Agreement includes the standard contractual provisions for acquiring services (e.g., the scope and standards of services to be provided, clear performance metrics, regulatory compliance, reporting obligations, term and renewals, dispute resolution, and the calculation of the cost of service, including operational and capital considerations).

The table below illustrates the differences between the current responsibilities of the City Council and those following the implementation of the MSC model. With the introduction of the MSC model, the City Council would maintain ownership of the assets as a shareholder of the corporation, provide guidance on strategic policy direction, and appoint the Board of Directors. However, it would no longer retain direct responsibility for approving budgets.

City Council Responsibility Current State Future State Ownership of water and wastewater assets ✓ ✓ Approving service rates ✓

✓ Approving operating budget ✓ Approving capital budget ✓ Strategic policy direction ✓ ✓ Appointment of Board of Directors (as per Shareholder Declaration) ✓ ✓ Allocation and Collection of Development Charges ✓ ✓ Approving the use of alternative financing tools (e.g., debt instruments, bonds, etc.) ✓ Financial Structure

A number of questions and concerns have been raised about the City’s motivation to establish an MSC.

The City’s primary objective is to establish a structure (MSC) that will have the capacity to take on its own borrowing and financing capacity. Currently Kingston Hydro is set up in such a way but Utilities Kingston, does not have the ability to undertake its own borrowing and financing. By establishing this MSC, the City would be able to transfer the water and wastewater debt which is about 40%-45% of the current city’s debt load so that future debt for water and wastewater is not impacting the City's debt capacity. The proposed MSC would have greater borrowing capacity and also access to different financing for repayment. This would allow the replacement of infrastructure and new infrastructure to be accelerated without adding to the City's debt burden.

The proposed MSC would be a corporation wholly-owned by a municipality, ensuring it remains under public control while allowing for operational flexibility, including the ability to access diverse funding sources. It would essentially act as a shell company which would hold assets, issue borrowing and ensure repayments while holding a service agreement with Utilities Kingston which would continue to operate day to day services related to water and wastewater. Funding sources available are development charges (DCs), revenue bonds and project-based loans. This approach allows for tailored financing that preserves operational independence and keeps debts off the City’s financial statements.

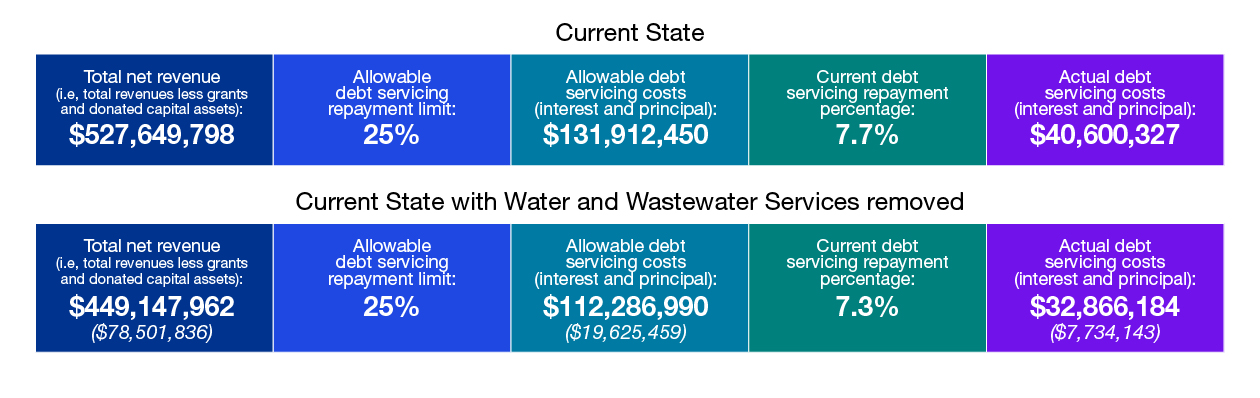

Ontario municipalities are limited with respect to the amount of long-term debt that can be issued based on a formula that caps debt servicing payments at 25% of net revenue. Based on the City’s 2024 Financial Information Return and 2024, the City’s debt servicing costs amounted to approximately 7.7% of net revenue. As a Government Business Enterprise, the revenues and debt servicing costs of water and wastewater services would be removed from the City’s financial statements thereby impacting the City's allowable debt limit.

Figure B: Financial statement comparison of current state and current state with water and wastewater services removed (including difference of amounts)